When selling services across borders, it is essential to determine the correct place of supply for VAT purposes. This identifies which country’s VAT rules apply and whether UK VAT should be charged. The rules differ depending on whether the transaction is business to business (B2B) or business to consumer (B2C), and there are several exceptions that depend on the type of service supplied. Getting this right ensures your VAT returns are accurate and that you remain compliant with HMRC and international tax regulations.

When cross-border sales take place, it is important to determine whether UK VAT is chargeable.

Business to Business (B2B) supply of services

The general rule for B2B supplies of services, is the place of supply is where the customer ‘belongs’ eg. where the business customer is established. For a UK supplier, providing services to an overseas business customer, these sales are therefore outside the scope of UK VAT. These sales do not count towards the UK VAT registration threshold.

There are, however, seven services where special place of supply rules for VAT apply, as follows:

|

Type of service

|

Place of Supply

|

|

Land-related services

|

The location of the land

|

|

Passenger transport

|

Where the journey takes place

|

|

Admission to events and related services

|

The location of the event

|

|

Restaurant services and catering

|

The place of consumption of the food

|

|

Short-term hire of a means of transport

|

Where the customer takes delivery

|

|

Telecoms, broadcasting, hire of goods and electronically-supplied services

|

Where the service is used and enjoyed

|

|

Freight transport, wholly outside of the UK

|

Location of the journey

|

Taking land related services as an example, in the circumstance of a UK supplier supplying land-related services to a US supplier relating to land in the UK, UK VAT is chargeable. This overrides the general rule of the place of supply being where the customer is established.

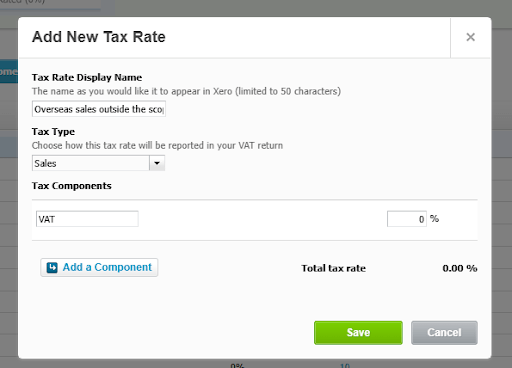

How do I account for these sales in Xero?

In the case of B2B overseas sales, which are not subject to UK VAT, but would have been subject to VAT had they taken place in the UK, they are out of scope of UK VAT but not out of scope of VAT altogether. It is therefore not appropriate to use the ‘no VAT’ code in Xero.

The zero rated VAT on sales code is often used, however this is still not technically correct under VAT law. Therefore, an alternative and better approach is to set up a custom VAT code in Xero to capture these sales.

A custom VAT code can be set up by selecting the tax menu, and then tax settings, and completing the pop up form. The new VAT rate should be given an appropriate name eg. ‘overseas sales outside the scope of UK VAT’, the tax type set to sales, and the VAT rate selected as 0%.

The sales will then show on the VAT return, with no VAT applied.

This tax code should be applied whichever country the business customer resides in, providing the general rule of being outside the scope of UK VAT applies.

Services which are exempt from VAT eg. insurance do not fall under this treatment, and continue to be treated as exempt in Xero.

Business to Customers not in business (B2C) supply of services

The default position for B2C supplies of services is that the place of supply is where the supplier is established. Therefore in the case of a UK business supplier providing services to a French consumer, it is likely that UK VAT will be chargeable. B2C services cover services to customers not in business, which covers consumers as well as other organisations, such as charities not in business, or overseas government organisations.

However, there are a number of exceptions to this default position.

Some service B2C supplies have a place of supply where the service is performed:

- Work on goods

- Valuation of goods

- Cultural

- Artististic

- Sporting

- Scientific

- Educational services

- Entertainment services

- Freight transport, point of departure

B2C Broadcasting, e-services and admission to a live online event or training course is deemed to have a place of supply where the customer belongs.

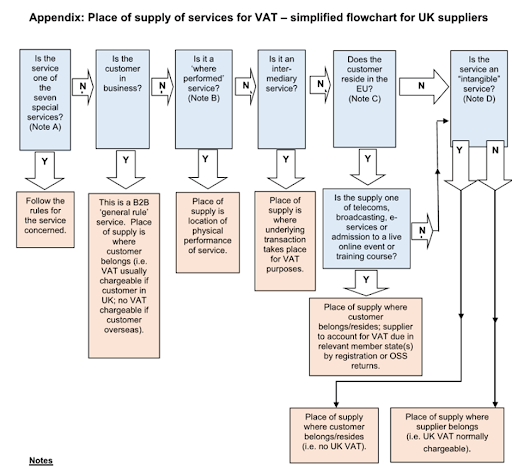

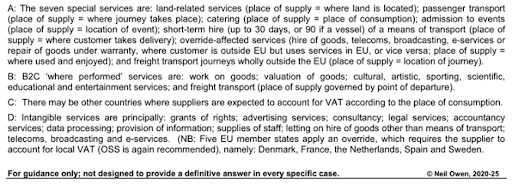

Please see the flowchart from Neil Owen (Innovation 2020 training) below for more details

These areas can be complex; please seek advice when there are uncertainties.

Where the place of supply for B2C consumers is in the EU, the UK supplier is required to join the non Union One Stop Shop, in order to report and pay over the VAT due on these sales. Registration is required in an EU member state, and therefore it is recommended that UK businesses register for the non Union OSS in The Republic of Ireland. Returns are then completed quarterly, just as in the case for VAT returns.

Read our full guide on accounting for value added tax (VAT) to learn more.

If you need help with this, or with other advice, then please get in touch with our accounting team.