Exchange rate movements are recognised in Xero as either realised currency gains or losses or unrealised currency gains or losses. But how are currency gains and losses accounted for in Xero? Here is our full accounting guide.

Realised currency gains or losses

This currency movement is recognised in xero when an invoice in a foreign currency is paid. The difference in the exchange rate between the date of the invoice in xero, and the date the invoice is paid is calculated by xero automatically and posted to the realised gains account.

The ‘Realised Gains and Losses’ report can be run from the reports menu, to show the amounts which make up the balance of the realised gains account (accounting-reports-search ‘realised gains and losses’).

The report shows, for both accounts receivable and accounts payable, the details of the invoice, the currency used, the source amount, and the exchange rates at both the invoice date and the payment date, to give the exchange rate difference posted. Please see the below example for a sales invoice in US Dollars.

Unrealised currency gains or losses

Xero uses the unrealised currency gains account to revalue all the foreign currency balances in accounts receivables and accounts payables as at the report date. For example, the profit and loss account run for the month of March 2025 will show the potential gain or loss on all the foreign currency transactions still to be paid at 31-03-2025, based on if they were to be settled at the exchange rate in effect at that date. This is to reflect in the accounts, the fact that previous invoices will no longer be recoverable or payable at the original converted sterling cost, due to movements in the exchange rate.

A summary report of the unrealised gains or losses by currency can be obtained from the reports menu (accounting-reports-search ‘foreign currency gains and losses’), or by selecting the figure on the unrealised currency gains line on the profit and loss account. Individual figures in the unrealised gain column on the report can then be selected to drill down into the detail by outstanding invoice.

Can I edit the exchange rate in Xero?

Exchange rates are updated in Xero hourly, using XE.com as the source. The official rate for the day is the final rate at 11pm. However, there may be instances where you know the exact exchange rate for a transaction, for example where you have forward bought currency to cover specific transactions. In this case the exchange rate can be edited for a date, a date range or specific transactions.

To edit an exchange rate for a date:

- select Settings in the organisation menu.

- Select Currencies

- Select the date to edit in the dropdown box.

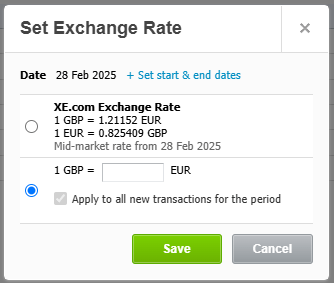

- Select the specific currency units per GBP, in the example below of 28 February 2025

- The default will be the XE.com exchange rate. Select instead the 1 GBP = EUR rate, enter the correct exchange rate in the box, and save.

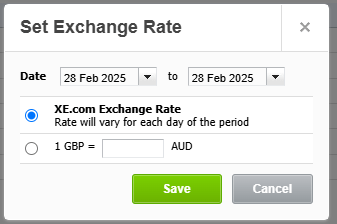

If the exchange rate is to be set for a specific period of dates, please select the ‘+set start and end dates’ option in blue at the top of this box, and enter the correct from and to dates, shown in the example below for 20th February to 28th February 2025.

To edit an exchange rate for a specific transaction:

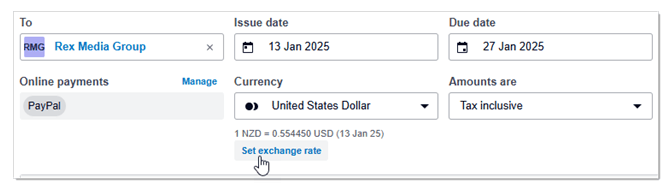

For invoices, click on ‘Set exchange rate’ in blue at the top of the invoice form, and select ‘Custom exchange rate’ to enter the correct exchange rate.

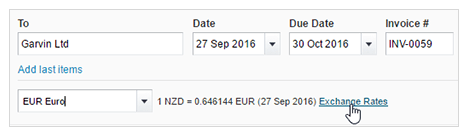

For bills, credit notes, or spend or receive money transactions, click ‘Exchange rates’ shown in blue on the input form, and again select ‘Custom exchange rate’ to enter the correct exchange rate.

If you need help with this, or with other advice, then please get in touch with our accounting team.